Understanding how credit scores are calculated can sometimes feel like unraveling a complex puzzle. However, breaking down the key components gives a clearer picture of how these scores are derived and what they signify. A credit score is essentially a numerical representation of your creditworthiness, influenced by various financial behaviors and patterns. This guide will delve into the factors that impact your credit score and explain how each element contributes to your overall rating.

What is a credit score?

A credit score is a numerical representation of your creditworthiness. It is calculated based on your borrowing and payment history and indicates to lenders how likely you are to repay your debts on time.

It’s also important to understand that you don’t have just one credit score—different lenders and credit reporting agencies use multiple credit scores. While most scoring models assess similar factors such as payment history, amounts owed, length of credit history, new credit, and types of credit, they may weigh these factors slightly differently, resulting in variations in your score.

How is a credit score calculated?

The most common credit score you’ll hear of is FICO or the Fair Isaac Corporation. FICO determines the creditworthiness of an individual with a number, typically between 300 and 850. This FICO credit score is the lending industry standard for making credit-related decisions.

FICO scores are calculated from information pulled from the three major credit bureaus in the United States: Experian, TransUnion, and Equifax. These bureaus, in turn, gather information from lenders like credit card companies, student loan lenders, and banks.

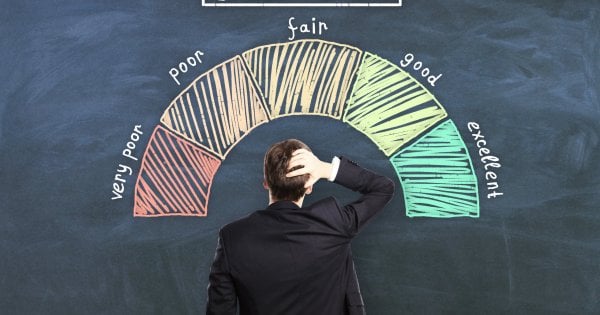

FICO credit scores are divided into several ranges that help lenders assess an individual’s credit risk. Here’s a breakdown of the different ranges:

- Very Poor (300-579)

- Fair (580-669)

- Good (670-739)

- Very Good (740-799)

- Exceptional (800-850)

Your personal credit score has a large impact on your ability to get a business loan. Most lenders will have a minimum credit score requirement in addition to other eligibility criteria.

FICO determines your credit score based on five factors, but each is weighted differently. Your repayment history and overall credit utilization are the main components of your score.

5 components of your FICO credit score.

1. Payment history

FICO says that payment history determines 35% of your credit score, making this factor the most important aspect of your credit reports. The guiding wisdom here is that past repayment behavior is the best way to determine your ability to pay off new debts.

“Both revolving credit (i.e., credit cards) and installment loans (i.e., mortgage) are included in payment history calculations, although installment loans take a bit more precedence over revolving credit,” financial expert Rob Kaufman of FICO writes. “That’s why one of the best ways to improve or maintain a good score is to make consistent, on-time payments.”

You can boost this portion of your score, and, therefore, greatly boost your FICO credit score overall, by paying down existing debts. One of the fastest ways to push your score skyward is to pay off a debt like a credit card completely. Even ensuring your payments are timely can have an impact, although paying above the minimum will compound your efforts to improve your score.

2. Amounts owed

The next biggest factor FICO uses in determining your credit score is your “credit utilization.” As the term suggests, this metric compares the amount of credit you are using to the credit available to you. This factor accounts for 30% of your FICO score.

Basically, your credit utilization is the percentage of debt you carry. If your credit burden is high, it will lead lenders to believe that much of your monthly income is going toward debt repayments.

“Credit score formulas ‘see’ borrowers who constantly reach or exceed their credit limit as a potential risk,” Kaufman explained.Generally, a “good” credit utilization ratio is 30% or less. Improving this aspect of your credit score can require some strategic thinking. If you pay off a credit card, you might want to keep that account open so the open credit line pushes the ratio in your favor. Similarly, asking for credit limit increases can better your burden percentage.

3. Length of credit history

The number of years you have been using credit has an impact on your score. FICO says it makes up 15% of your score, although this can be a bigger factor if your credit history is very short.

“Newer credit users could have a more difficult time achieving a high score than those who have a credit history,” Kaufman said, “since those with a longer credit history have more data on which to base their payment history.”

It’s smart to always have some lines of credit open, even if you aren’t using them. This approach is especially true if you, or your children, are young adults, although you want to ensure you can responsibly handle credit cards.

4. Credit mix

Credit mix accounts for 10% of your FICO score, so it is a relatively minor factor unless your credit history is limited. Generally, lenders like to see several different kinds of lines of credit on your report, like credit cards, student loans, auto loans, and mortgages.

“Credit mix is not a crucial factor in determining your FICO score unless there’s very little other information from which to base a score,” Kaufman stated.

If you have multiple lines of credit open, you probably don’t have to worry about this factor. Instead, focus on changing your credit utilization ratio or improving your repayment history.

5. New credit

The final 10% of your FICO score is determined by how many lines of credit you have opened recently. This aspect is why people say hard checks on your credit score can actually hurt your standing.

“Opening several new credit accounts in a short period of time can signify greater risk—especially for borrowers with a short credit history,” said Kaufman.

When you apply for a new credit card, loan, or lease, lenders look at your credit history. This check itself shows up on your credit report, even if you were denied the line of credit.

Inquiries can remain on your credit report for 2 years, but FICO only includes credit checks made in the last 12 months in determining scores. “Soft” checks on your credit, like credit monitoring services, are not included.

Read the full article here